Exchange rate and time

Last Sunday New Zealand and Samoa just switched from standard time to daylight saving time (DST). In the next few weeks, Paraguay is also set to switch to DST. Let me clarify, though, that this article is not about a call for the Philippines to adopt DST. DST was actually enforced for a short period in the 1990s to alleviate the energy crisis the country was experiencing then. However, as our power generation and transmission capacities improved, the practice was subsequently abandoned.

Rather, this article is about sharing my personal take on the peso, which has been the talk of the town of late. It would also be useful to take these events to bring up Milton Friedman’s striking analogy between flexible exchange rates and, of all things, the DST.

In 1953 Friedman reminded everyone that instead of changing our behavior or daily habits in line with the waxing and waning of the extent of daylight hours, it was simpler to adjust our clocks. Analogously, he argued that rather than altering wages and prices, it was simpler to adjust the exchange rate accordingly. (1)

Barking up the wrong tree

This brings me to my main point about the recent developments of the peso—the issue is not so much about whether the peso is weak or strong; it is about the ability of the exchange-rate regime to effectively adjust to the varying economic conditions and serve as an automatic stabilizer. When the peso needs to be strong or weak, depending on the business and financial cycles being reflected on the balance of payments, and it is able to swing as needed, then we should take comfort in the fact that this would be a positive to the economy.

In my view, pundits and market observers are barking up the wrong tree by focusing on the peso’s direction of movements. While most of these articles’ arguments have merit, fixating our analysis on the domestic currency’s direction is one-sided.

To illustrate, we can ask ourselves what is preferable: a firmer or a weaker peso? Each has its own advantages and disadvantages. On one hand, a firmer peso would favor consumers by tempering the general rise in the prices of goods and services. On the other hand, a weaker peso would favor certain sectors in the economy, such as exporters, foreign investors, and recipients of overseas Filipino workers (OFW) remittances.

What we need is a flexible exchange rate that would depreciate when our exports are losing external competitiveness and our OFWs are losing on their remittances due to previous appreciation. Likewise, if the peso has depreciated and exports and investments start coming in, some strengthening would be required to restore equilibrium.

In other words, a peso depreciation or appreciation will always have winners and losers. Hence, from a policy standpoint, it is more useful to focus on the peso’s flexibility to absorb shocks to the domestic economy and restore macroeconomic balance.

Exchange rate as an automatic stabilizer

The exchange rate acts as an automatic stabilizer or shock absorber if it moves in a way that dampens the effects of global shocks on domestic output. To say the obvious, currency depreciation at a time of slowing growth should stabilize economic activity (say, by boosting exports, curbing imports or some combination of both). In theory, this adjustment takes place through income and expenditure-switching effects.

Income effects could arise following a depreciation, as the depreciation provides the economy less purchasing power abroad. To tighten belts in the face of reduced income, domestic demand and imports will drop. Additionally, the movement of relative prices can trigger a series of expenditure-switching effects that reshuffle production and spending across goods and countries. As foreign goods become less affordable, domestic consumers shift toward cheaper domestic alternatives, supporting local output. And as export products become cheaper in dollar terms, they become more affordable to foreign buyers. To the extent that exchange-rate flexibility is a conduit for expenditure-switching effects, it can provide a key buffer for small open economies facing external shocks, by boosting exports and supporting domestic demand and output.

When less means more

In terms of flexibility, the Bangko Sentral ng Pilipinas (BSP) continues to adhere to a market-determined foreign-exchange policy. In other words, we do not fix the exchange rate at a given level but instead we allow the interplay of supply and demand for the currency to determine the exchange rate. Contrary to other claims, the BSP does not target a particular level of exchange rate nor drag down the peso to a particular level. The BSP’s participation in the foreign-exchange market (by either buying or selling dollars) is limited only to ensuring orderly conditions and avoiding unnecessary swings in the exchange rate or when volatility in the foreign-exchange market is excessive. This type of policy mix has been shown to be effective not only in pursuing macroeconomic stabilization and anchoring expectations, but also in reinforcing the credibility of inflation targeting. (2)

It is not constructive to be making reference to the BSP dragging the peso to 40 from more than 50 a few years ago. No central bank can do that without losing its shirt or upsetting market fundamentals, with durable results.

Our choice of foreign-exchange policy is dictated by the impossible trinity that states that a central bank can only pursue two of the following objectives: fixed exchange rates, independent monetary policy and open capital account. Thus, in the advent of globalization where capital can flow freely, gaining monetary independence entailed allowing market forces to determine the exchange rate. Interestingly, based on my many years as a central banker, the limitation imposed by the impossible trinity could actually work to our advantage.

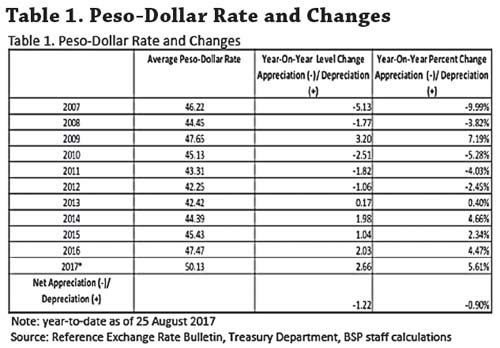

A quick look at the peso’s movements from a longer horizon will show us that the peso’s movement has broadly reflected prevailing macroeconomic conditions (Table 1). To elaborate, the fiscal reforms in mid-2000s raised investor confidence in the country. This resulted in a higher demand for the peso following the surges in the inflow of capital, direct investment and remittances. All of these actually led to an appreciation of the peso from an average of 51.35 per $1 in 2006 to an average of 44.45 per $1 in 2008.

Likewise, in the aftermath of the global financial crisis (GFC), quantitative easing (QE) policies of advanced economies’ central banks led to dollar inflows to small emerging markets including the Philippines (2010-2012). By 2012, the peso appreciated to average at 42.25 per $1.

Between 2013 and the present, expectations of recovery in advance economies and the corresponding rise in their interest rates have increased preference for dollar-denominated assets, resulting in greater demand for dollars in the domestic economy. These dollars were part of the capital that has flown back gradually to advance economies.

Recent peso developments

In line with these developments, the peso’s current depreciation can be due in part to the country’s growth momentum. The Philippine economy is growing and it can be expected that this will be accompanied by stronger demand for imports, reflecting the sustained rise in business and production activities to support economic growth. Moreover, many companies have started to repay and prepay their FX debt obligations, some have started to invest outside the Philippines. These, in turn, would also explain the peso’s recent depreciation.

Is this surprising?

On a year-to-date basis, the peso depreciated against the US dollar by 2.83 percent to close at 51.17 per $1 on August 31, 2017, from the closing rate of 49.72 per $1 on December 29, 2016. At first blush, the peso’s depreciating trend may appear unique relative to neighboring economies. However, the peso’s year-to-date depreciation may hardly be comparable to the generally appreciating trend of other currencies since observed trends vary according to the reference dates being used. In fact, over a five-year period, the peso movement is not unique and its depreciation trend is consistent with other Asian currencies (Chart 1).

In real terms, the peso’s performance has shown relative stability over the years. This is particularly true when looking at the trend in the real effective exchange rate (REER) of the peso versus a basket of currencies. The REER, by the way, is one way of evaluating the appropriate level of the exchange rate since this measure takes into account not only the nominal exchange-rate movements but also the relative inflation rates among trading and competing countries.

Chart 2 shows that the REER index of the peso against the basket of currencies of all trading partners (TPI, blue line), trading partners in advanced (TPI-A, red line) and developing (TPI-D, green dash line) countries has been broadly stable.

Benefits of flexible exchange rate

Indeed, the flexibility of the peso has provided our economy an effective mechanism to cope with shocks. Chart 3 shows how flexible exchange rates could perform this role. The horizontal axis refers to year-on-year changes in the International Monetary Fund’s (IMF) World Economic Outlook (WEO) GDP Forecast for the Philippines (proxy for output shocks), while the vertical axis refers to percent changes in the nominal peso. The chart shows that when output surprises on the upside, the peso appears to act as a buffer and tends to appreciate. Conversely, when output shock is negative, the peso tends to depreciate. Interestingly, out of 44 instances, the peso has adjusted correctly (or as expected) 27 times.3 These suggest that, in most cases, the peso acted as a buffer during output shocks.

Chart 3. Exchange Rate and GDP Forecast Revisions

Actual data shows how the flexible exchange- rate regime has helped the country achieve 74 consecutive quarters of positive GDP growth since Q1 1999 (a span of 18 years). Moreover, our flexible exchange-rate policy worked well with inflation targeting framework as characterized by the low, stable and on-target inflation environment since the adoption of the IT framework (except during the global financial crisis 2008-2009).

Embracing flexibility

These benefits show that our foreign-exchange policy of flexible exchange rates continues to be relevant and appropriate. The peso’s flexibility, in more ways than one, has allowed us to reap the benefits of structural reforms that we have put in place in pursuit of sustainable growth. Rather than concentrating on achieving a weaker or stronger peso, it is flexibility that we must support.

Let us not forget Lao Tzu who said:

“Whatever is flexible and living will tend to grow; whatever is rigid and blocked will wither…”

1 Friedman, Milton (1953). “The Case for Flexible Exchange Rates,” as cited in “International Money: A Collection of Essays” by Charles P. Kindleberger.

2 Alla et al., 2017, “FX Intervention in the New Key-nesian Model” IMF Working Paper, September 2017.

3 Instances when peso adjustment deviated from the correct direction could potentially be due to other factors.